(Psst: The FTC wants me to remind you that this website contains affiliate links. That means if you make a purchase from a link you click on, I might receive a small commission. This does not increase the price you’ll pay for that item nor does it decrease the awesomeness of the item. ~ Daisy)

By the author of The Ultimate Guide to Frugal Living and The Flat Broke Cookbook

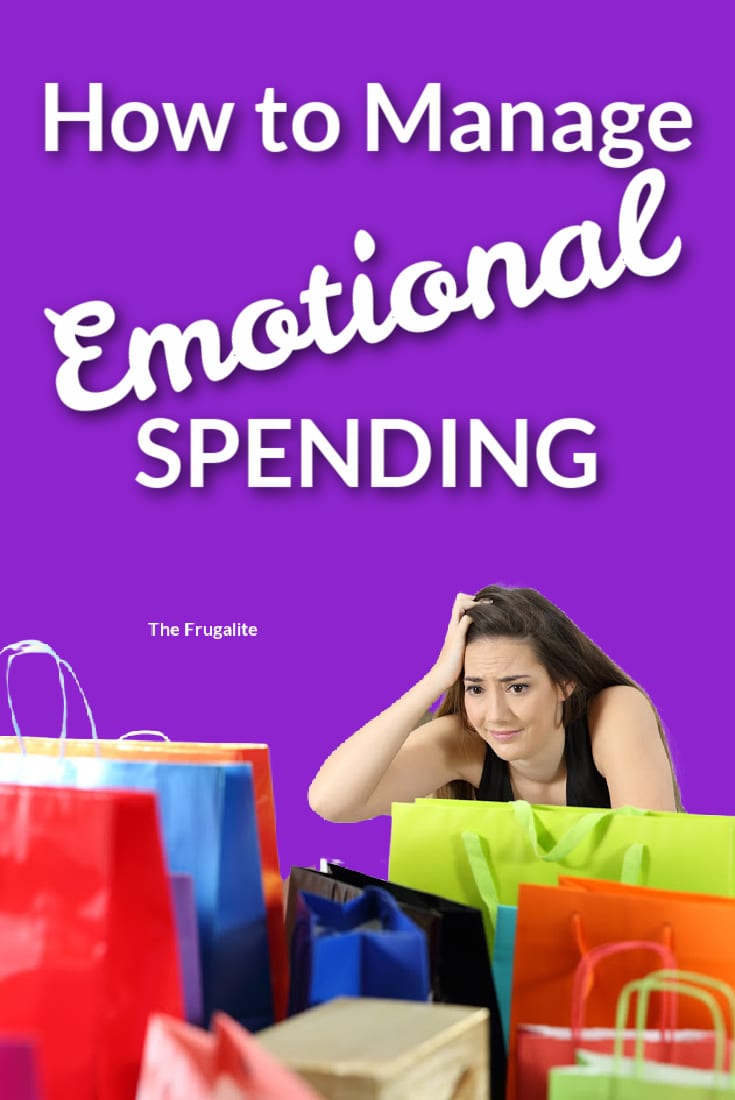

Are you happy? Go buy something to make a good day even better.

Are you sad? Go buy something to cheer yourself up.

Are you having a rough day? Go buy something because, darn it, you deserve it.

Are you angry? Go buy something to distract you from your rage.

Did you just accomplish a goal? Go buy something to celebrate.

Are you feeling alone? Go buy something to take your mind off your loneliness.

Does this sound familiar? If it does, you may be an emotional spender. And if you are, you’re not alone. Half of the Americans surveyed in 2017 admitted to emotional spending, and many of them said it had led them to being deeper in credit card debt. Given that human nature is human nature, I doubt that the statistic is that far off still in 2023. As Chloe Morgan wrote in an article, mental health and money management are closely linked.

If buying things is your go-to mechanism for dealing with your emotions, how do you STOP? These ideas can help.

Come up with some no-spend rewards for yourself.

This could be one-on-one time with a loved one or close friend, a long hike on a Saturday afternoon, a trip to the park with your children, visiting the museum on free admission day, a visit to the animal shelter to pet the dogs (this can be dangerous if you’re anything like me – you might come home with a pet!), a trip to the library for some good books, or performing volunteer work that makes your heart feel full. I like to sit down and watch a movie on Netflix or Amazon Prime as a reward after a long day. I wrote more about no-spend treats in this article.

Kibosh impulse spending.

This isn’t easy, but you’re going to have to delay your gratification for a while. When you see something that you weren’t planning to buy, and you suddenly want it like crazy…STOP. Stopping doesn’t mean you’ll never get it. It means that you’re going to think it through and make sure you truly want it.

Give yourself 24 hours to think it over.

- Will it harm your budget?

- Will it cost you even more money to maintain the item?

- Will you be paying it off for years?

Make your spending choices very consciously and not impulsively.

Unsubscribe.

Does your inbox look like mine? Is it full of newsletters from retailers who breathlessly announce “the best sale ever” on a daily basis? It’s hard to say no to those all the time. Think about it – they’re written by marketers who spend years learning to part you from your money.

Unsubscribe. Yes, you’ll probably miss out on some deals, but if you need to go to a store, you can usually find the same coupons that would go to your inbox available to download online. Trust me, you don’t need the constant barrage of temptation. I recently unsubscribed from 98 – count ‘em – 98 retail email lists. What a relief! Here’s an entire article I wrote on the importance of unsubscribing.

Avoid places that make you want to spend money.

For me, it’s Home Goods and TJ Maxx. I simply cannot walk into those stores and walk out with nothing. It’s all so pretty, so unique, so MUST-HAVE-THIS-IN-MY-LIFE that I rarely escape unscathed.

So, I just don’t go there. If I DO go, it is with cash that I have put aside for this specific purpose. I leave my debit card at home and that way I can’t be tempted to purchase things I don’t need. Your own can’t-resist store may be different – it may be the whole mall – but whatever it is, you can’t spend money there if you don’t go.

Don’t save your credit card information on online stores.

This is a hard-learned lesson from Amazon. The added step of putting in my card each time keeps me from just hitting one-click purchase and ending up with a lot of frivolous things in my mailbox.

Amazon can be the source of many great purchases, but it can also be the biggest expense on your credit card bill.

Kick cable TV to the curb.

I’ve used streaming services like Netflix for so long that I’d completely forgotten what it was like to see the barrage of commercials until I visited a family member who has cable. Every 10 minutes, 3 or 4 commercials were urging me to spend money, buy fast food, or save the dogs in an NYC shelter. Why put yourself through that?

Folks in advertising are professionals at parting you with your money, and those ad spots cost millions of dollars, so you’re trying to resist the very best.

Block ads online.

Of course, the internet brings commercials right to you through all sorts of nefarious methods, like cookies from websites you’ve visited. Try AdBlock or some other method to keep those ads from flashing before your eyes on every website you visit.

Heck, even email services like Yahoo have ads on the sidebar based on your internet habits.

Figure out what’s going on in your head.

If you’ve been overspending recently or feeling out of control with regard to money, what is going on in your life that is making you feel this way?

Introspection isn’t often fun, but it can be necessary. When you pinpoint the real problem, then you need to search for a solution to it (assuming there is one – that isn’t possible in every case.) If a solution isn’t possible, then you need to plan for best- and worst-case scenarios. Personally, I always feel better when there’s a plan. You must create new habits.

If emotional spending has always been your go-to response, it will take some time to create the new habits that you desire. But it can absolutely be done.

- Know your triggers.

- Have fiscally responsible substitutes ready.

- Practice, practice, practice.

Don’t beat yourself up too much if you backslide – we’re only human! You’ve got this!

Do you have issues with emotional spending?

How do you prevent emotional spending? What are your triggers? Let’s talk about it in the comments.

About Daisy

Daisy Luther is a coffee-swigging, adventure-seeking, globe-trotting blogger. She is the founder and publisher of three websites. 1) The Organic Prepper, which is about current events, preparedness, self-reliance, and the pursuit of liberty; 2) The Frugalite, a website with thrifty tips and solutions to help people get a handle on their personal finances without feeling deprived; and 3) PreppersDailyNews.com, an aggregate site where you can find links to all the most important news for those who wish to be prepared. Her work is widely republished across alternative media and she has appeared in many interviews.

Daisy is the best-selling author of 5 traditionally published books, 12 self-published books, and runs a small digital publishing company with PDF guides, printables, and courses at SelfRelianceand Survival.com You can find her on Facebook, Pinterest, Gab, MeWe, Parler, Instagram, and Twitter.

{kind=link}

3 thoughts on “How to Manage Emotional Spending”

I must have the frugal gene (long, long line of farmers). I always think twice about spending money (charitable contributions are budgeted). One thing I instilled in my kids is the “how many hours do you have to work to NET the amount of money required for an item?”. Granite countertop in the kitchen would cost more than ALL the countertops required in my home. Granite wasn’t a good choice for us (IMHO, granite is for those who don’t cook much at home, if at all). So other options for me, under budget. Want vs. need is difficult for even the most disciplined person. One can be penny wise and pound foolish but that is to be avoided. Bookstores are my Achilles heel. What I pay for a library card (those in my area wouldn’t pay $2 a year for the benefit of the library!) would pay for 4 hardback books (new). I find it helps to be “picky” on what/where one spends his/her money.

The unsubscribing is a big one in this electronic and non-brick and mortar age. A sucker for books, I can always “find” a bargain with a coupon. I have to remove myself from these lists to not even start there.

My favorite el cheapo way to use a local library (for books they don’t happen to have) is to check if a book title is at least 6 months older than the publisher’s date. If so (with a few exceptions like very rare books, reference books, or some antique books) they are fair game to request a free (or nearly free) interlibrary loan — a system that’s been in use in the USA since before 1900. That can give you a few free weeks to read the book or just skim through it to see if that reading was enough for you or if (for a small minority of titles) it’s worth it for you to purchase one. For the few who might be high volume book readers … there is a global community of readers who legally use either book scanners bought at retail or make their own book scanner via a DIY process. The DIY community is here: https://www.diybookscanner.org/ Since the copy they make is for their own personal use … they are not violating copyright law.

The legal protection for debit card purchases has improved somewhat. I prefer them for multiple reasons. I don’t have to figure out a monthly total and mail in a check to my credit union. I can also create a virtual charge card number for it for any single seller (or group of sellers that I choose) via the free privacy.com service … so that a scammer who learns your virtual card number can’t use it with any seller you didn’t specify. Another benefit will be obvious from a recent charge I didn’t recognize in the mid-$900s range. Whether it was from a fine print hidden automatic renewal subscription agreement or a scammer’s use of it … I had zero knowledge. So when I explained that to my credit union … they contacted the seller which then reversed that charge completely. If you stick to only one vendor per virtual charge card number … that will help minimize such problems. Another way to minimize problems with highly sneaky and often fine print hidden automatic renewal charges is to change your charge card annually … and only disclose the new number (or the new virtual card numbers) to the minority of vendors you choose … or simply terminate the virtual card numbers for the vendors you wish to forget about.

Another way to defend against charge card number theft is to pay in cash in person. That way no electronic skimmer stuffed into a retailer’s checkout equipment (like a gas station pump, etc). The majority of such charge card usage theft comes from such skimmers … and not from electronic sniffers carried by a bad guy just passing by you.

Back to the emotional spending problem. I find that waiting at least a day (ie., sleeping on the matter) relieves much of the emotional kick the retailers are expert at creating. Another management tool (at least for sellers you only infrequently buy from) is to create a virtual charge card number (as described above) and then shut it down after even one such purchase. Then if you don’t need to buy from that seller for, say a few months, or maybe even longer, only create a new virtual card number for that vendor once it is finally needed. … and then decide if you might not need to buy from them for a few months or even a few years … after which it might become worthwhile to create a replacement virtual number for that vendor when the need arises. Again … time removes much of the emotional tug the vendor hopes will entrap you.

–Lewis