(Psst: The FTC wants me to remind you that this website contains affiliate links. That means if you make a purchase from a link you click on, I might receive a small commission. This does not increase the price you’ll pay for that item nor does it decrease the awesomeness of the item. ~ Daisy)

The problem with poverty in America is that the system is designed to keep you poor. Maybe it’s just because poor people are easier to control. I have written before about how to survive when you’re so broke that you can’t pay your bills and while the comments were largely supportive, there are always a few smug, superior souls who blame the people who are struggling for their problems. The thing is, poverty is a trap, and one seeming small setback can spiral into a disaster from which you cannot extricate yourself.

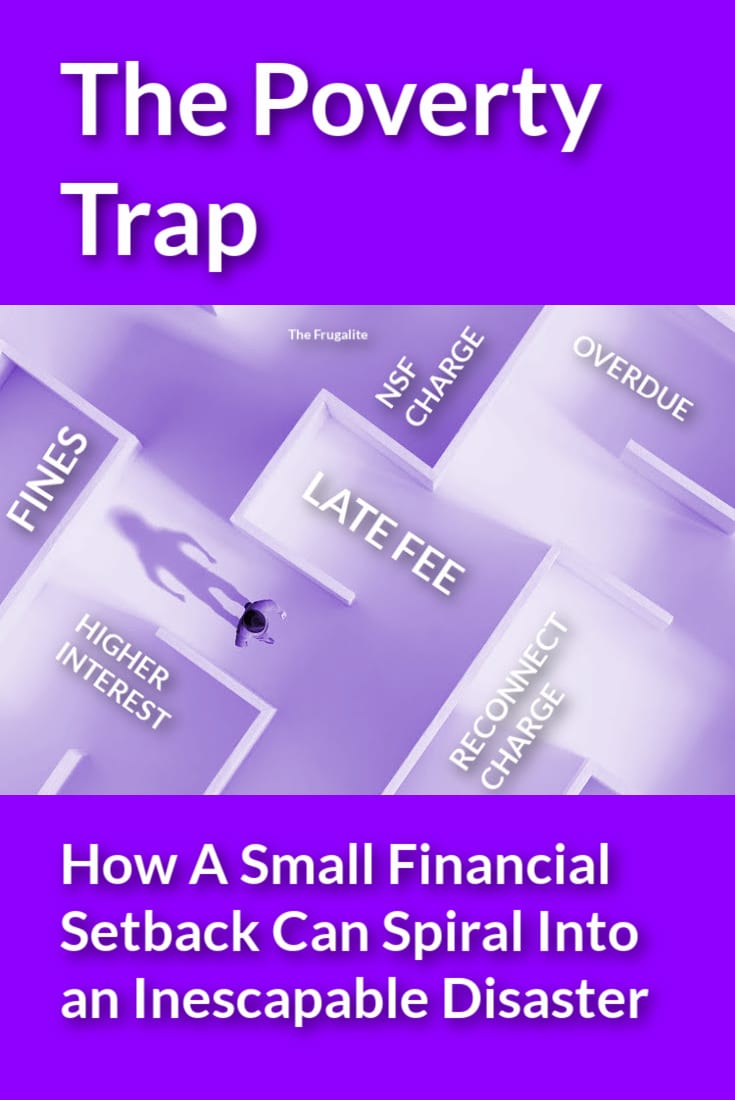

When you are living a financially fragile life, it seems like someone somewhere is trying to keep you poor. Why is it so hard to get ahead? Well, because the system is rigged against you when you’re living paycheck to paycheck with fee after fee after fee. Because what makes more sense than charging someone who already can’t pay their bills even more money?

Land of the Fee

First, there are the fees. We’ve written here about undisclosed fees that most people are being hit with, but bank fees are even worse.

If you bounce a payment by so much as a penny, then you are hit with a charge from your bank and most times, a charge from the business that was taking the payment from your account. Most banks charge anywhere from $25-$38.50 when you have non-sufficient funds for a payment. Businesses charge in the same range, so that means that if one payment goes awry, you can lose $50-$77 in the blink of an eye.

Banks love NSF and overdraft fees. Why? Because in 2017, Americans paid $34 billion in fees for not having enough money to cover a payment.

Some of these fees come from the automatic payments that come from our accounts. Mortgage, car payments, insurance payments, and other bills are often automatically debited. Other fees come when a person has “overdraft protection” on their debit cards. This is when a person doesn’t have enough money in his or her account for a debit to go through but their credit union or bank covers it anyway.

The government’s Consumer Financial Protection Bureau explains just how insane these fees are. (Emphasis mine)

Today, the Consumer Financial Protection Bureau (CFPB) released a report that raises concerns about the impact of opting into overdraft services for debit card and ATM transactions. The study found that the majority of debit card overdraft fees are incurred on transactions of $24 or less and that the majority of overdrafts are repaid within three days. Put in lending terms, if a consumer borrowed $24 for three days and paid the median overdraft fee of $34, such a loan would carry a 17,000 percent annual percentage rate (APR).

“Today’s report shows that consumers who opt into overdraft coverage put themselves at serious risk when they use their debit card,” said CFPB Director Richard Cordray. “Despite recent regulatory and industry changes, overdrafts continue to impose heavy costs on consumers who have low account balances and no cushion for error. Overdraft fees should not be ‘gotchas’ when people use their debit cards.” (source)

So to be clear, the banking system is set up to take the most money from people with the lowest balances.

One NSF or overdraft fee can unleash financial chaos.

Imagine you have a bill that attempts to debit from your account twice, costing you $50. Then another payment, a smaller one, that would have gone through if the other bill hadn’t gotten there first, bounces too. Now you’ve lost $75. It’s pretty easy to see how another payment – even one for a few bucks, could bounce next. Now you’ve lost $100.

By the time you actually have the money to cover all the fees, how on earth are you supposed to pay the bill that put you in the negative in the first place?

I know what a lot of you are thinking. “I’ve never bounced a check in my life” or “these people need to get control of their spending and they wouldn’t have these fees.”

But this vicious spiral can be caused by something as seemingly trivial as a person’s pay being direct-deposited one hour late on payday. It can occur when payday is on a Saturday but your funds won’t be deposited until Monday but your debits are still coming out regardless that it’s a weekend. It isn’t always personal irresponsibility that causes a person to be unable to cover the payments coming out of his or her account.

Once you’re in the hole for a couple hundred dollars in NSF or overdraft fees, how in the world do you get out? If your financial situation is so precarious that one bounced payment causes this cartwheel of non-sufficient funds, how are you supposed to ever get caught up?

And that’s not the only fee a person struggling financially can expect.

Next, there are late fees and the re-connect fees.

If one of the payments that went awry in your overdraft avalanche happens to be a utility bill, things get even worse for a person who is struggling. Particularly if you aren’t able to cover the bill in sufficient time to keep your utilities from getting shut off. How much you’ll be charged varies by company but if they really feel like you’ll have trouble paying in the future, they stick it to you, making it nearly impossible to get your power or heat turned back on. Here are some examples

- PG&E: “To restore service, you must pay the full amount due. You may also be required to pay a deposit twice your average monthly bill to re-establish credit.”

- Coast Electric: $35-50 fee to reconnect service, $6.50 late fee, $35 NSF fee, and potentially even a $35 collection fee

- Talgov: $28.50 each for gas, water, and electric

They can be charged late fees by all sorts of businesses. Now they’re really in trouble.

Heaven help you if have an unexpected bill.

If your budget is incredibly tight and you run into a bill that was unexpected, it can cause exactly the same upheaval as one of the fees mentioned above. This is why we recommend emergency funds so often, but what happens when that fund is gone? The past year has caused a lot of people to work through those hard-won rainy day accounts with nothing extra left for the unexpected.

What if your car breaks down? You know, the one you have to have to get to work. What if your refrigerator gives up the ghost? You know, the one with the meat you stocked up on in the freezer? What if your kid gets sick and needs to go to the doctor? Do you pay the $200 doctor bill or pay the electric bill?

These are the dilemmas formerly financially comfortable Americans are facing every day. I’ve been through it too – here’s my own story about living in poverty and it’s not a pretty one.

How do they bail themselves out of this mess?

A payday loan can be one way a desperate person chooses to get out of financial trouble.

Payday loans are short-term cash loans based on the borrower’s personal check held for future deposit or on electronic access to the borrower’s bank account. Borrowers write a personal check for the amount borrowed plus the finance charge and receive cash. In some cases, borrowers sign over electronic access to their bank accounts to receive and repay payday loans.

Payday loans range in size from $100 to $1,000, depending on state legal maximums. The average loan term is about two weeks. Loans typically cost 400% annual interest (APR) or more. The finance charge ranges from $15 to $30 to borrow $100. For two-week loans, these finance charges result in interest rates from 390 to 780% APR. Shorter term loans have even higher APRs. Rates are higher in states that do not cap the maximum cost.

CFPB found that 80 percent of payday borrowers tracked over ten months rolled over or reborrowed loans within 30 days. Borrowers default on one in five payday loans. Online borrowers fare worse. CFPB found that more than half of all online payday instalment loan sequences default. (source)

Now a bad situation has gotten even worse. You’re only getting a portion of your paycheck which means that you’re not going to be able to meet future bills. You’re going to face more late fees, more NSF charges, and more overdraft interest.

The cycle is vicious.

If you’ve ever wondered why broke people tend to stay broke, this is why. Unless the person in financial trouble gets some kind of windfall, they’re going to have great difficulty getting back on their feet. In many cases, it’s impossible.

And that isn’t the only bad part of the war on the poor. Homelessness has been practically criminalized. Here are some examples of how poor or homeless people can get in trouble with the law.

The criminalization of homelessness refers to measures that prohibit life-sustaining activities such as sleeping/camping, eating, sitting, and/or asking for money/resources in public spaces. These ordinances include criminal penalties for violations of these acts.

There are multiple types of criminalization measures which include:

-

- Carrying out sweeps (confiscating personal property including tents, bedding, papers, clothing, medications, etc.) in city areas where homeless people live.

- Making panhandling illegal.

- Making it illegal for groups to share food with homeless persons in public spaces.

- Enforcing a “quality of life” ordinance relating to public activity and hygiene. (source)

Of course, not all people financially struggling are out on the streets. Many are quietly struggling in middle-class neighborhoods, in nice homes, driving a late-model car. If they’re upside down in their mortgage or car loan, selling those items is not an option because then they’ll still be making the payments but be without a way to get to work or a place to live.

If they file for bankruptcy, good luck to them getting a cheap place to reside.

Things get harder.

And harder.

And harder.

How to avoid these traps

You may already be in financial trouble, or you may just be in a situation with no emergency fund. If that’s the case, you should know that it only takes something small to send you straight to financial disaster.

Here are a few tips to help you avoid the pitfalls of poverty.

- Don’t set up automatic payments. Some businesses force you to do this, but often you can cancel the autopay and pay yourself.

- Have one bank account for bills, and one for spending money. This way, you don’t accidentally spend money earmarked for utilities or your car payment.

- Don’t have overdraft protection on your account, particularly if the fees and interest rates are high.

- Don’t turn to payday loans. This is a cycle from which it’s nearly impossible to extricate yourself.

- Build an emergency fund. Even if you only put in $10 a paycheck, you’re still giving yourself a little bit of a cushion.

Know that you aren’t alone if you’re facing these kinds of problems. Many people in our country are deeply in debt, living paycheck to paycheck, and struggling to pay for basic necessities like food, rent, and medical bills. To add to our previous issues, the response to Covid has all but destroyed the personal finances of Americans.

Don’t look for things to become more affordable or for your paycheck to magically increase. That’s not the direction we’re going in America. Your only options are to reduce your expenses, eat cheaper food, and bring in some extra cash. If you get a windfall, use it wisely to build a financial cushion.

The American poverty trap keeps poor people poor. And it’s easier to fall into than you think.

Have you ever been trapped in this spiral?

Have you ever been in the delicate position in which one missed payment causes a cascade of fees, NSF charges, and other financial catastrophes? How did you recover? Let’s discuss it in the comments.

{kind=link}

20 thoughts on “The Poverty Trap: How A Small Financial Setback Can Spiral Into an Inescapable Disaster”

While I agree with pretty much all you said, I do disagree about one thing. For people with memory issues, whatever causes them, autopay can SAVE on fees. Believe me, I know. Before I had autopay, I spent an amazing amount on late fees, etc. Since I started using it, not one late fee, because I’m no longer relying on my ability to (a) remember that I have a bill to pay, (b) remember to write the check, (c) remember to put a stamp on the envelope, (d) remember to mail it. Or these days, remember to sit down with the bill and my phone and get online to pay it. The lower number of bills that aren’t on autopay, mostly medical, make it more likely that I will be able to get them paid before I get overwhelmed. Autopay can be a blessing or a curse, depending on your personal situation.

That’s a great point, Mary! I have a few things on autopay that are required, like my car payment and my insurance, but your logic is sound!

I set up auto pay through the credit union, not the debtor website. This, for me, is an added way to keep records of payment as well as keeping the company out of my bank account.

Your mentioning insurance reminded me of one year when we bought my wife a healthcare policy (don’t get me started on the issue of insurance being the wrong financial vehicle for healthcare) because it was far cheaper than what I could get through my employer. The company insisted that they be allowed to withdraw funds from my account. I was NOT going to give them access to my primary account, so I set up a secondary checking account at my credit union and gave them that one. I put money in to cover the bill and they stayed away from my main account. It cost me $1 per month, but was worth the security of mind.

With my bank, I have a credit card that I don’t use except that it serves to pay a bill that might come back NSF. I get a notice from the bank by email and I can pay the credit card immediately by shifting money around to pay it rather than have the card advance charge start building up. That bank is USAA. I’d never bank with BofA ever again!

I agree that autopay can be useful–especially if you live a busy life and can’t get to the post office to mail a bill on time. (I have quit using the postal drop boxes since I read an article about people putting long sticks into them with sticky tape on the end and pulling out mail–looking for checks, account into, etc. Who would have thought!) So I drive to the post office.

My husband and I do like to use a credit card for medical expenses (since you always have a record that you paid for that expense) and for gas. I have an automatic amount of money transferred out of my bank account into my credit card account each month, so I never forget to send in a payment. I have a tendency to put an envelope in my purse and forget to mail it, so for me this is helpful! I never have credit card late fees and my credit doesn’t take a hit. However, using a credit card can be really dangerous for running up expenses, so that may not work for everyone. Just what works for us.

Quite some years ago the local credit union I was using went through a strange election to become, or not, a bank instead. I believed at the time that some of the election claims being made were highly dishonest. Anyway, the change to a bank took place. A year or so later I made a dumb mistake and wrote some checks on the wrong (and minimal) account there — which I didn’t learn about until some weeks later when I finally received a bank letter about that damage to my PO box (more reliable than USPS drivers putting my mail in neighbors’ mail boxes) which I normally only check once or twice a month. In the meantime, the bank overdraft fees built up like crazy.

When I asked the now-bank if they were willing to notify me on a same day basis (if something like that ever happened again) by EITHER a phone call or an email, they simply refused. It was clear their new bank structure was designed to maximize any highly profitable overdraft damage. After that ugly conversation I withdrew all funds in cash from that bank and moved them over to a local credit union and never looked back. That bank was called on their sign the ViewPoint bank … which ever since I’ve only referred to them as the ScrewPoint bank.

–Lewis

I can vouch for everything you said Daisy, as I’ve lived with and I’m still living with it 20 odd years later. I blame no one but myself for my poor decision, but I will blame the system in place that perpetuates the financial repercussions inflicted years after the fact. The system isn’t designed to aid. It’s designed to enslave you in perpetuity.

It is what it is, and there’s not a damn thing I can do about it.

My (now deceased) husband had an account at a local bank where his social security check was automatically deposited 10 years ago. When deposit came in early because the normal date fell on a weekend he took the kids Christmas shopping. The bank charged him over draft fees for the whole weekend. $30 per store they visited. It added up to $200 over the weekend alone. By the time I found out about it, a week later, they had charged him another $300 in more fees over and above his fixed income. I had to pay it all back before I could close the account. They added fees daily even though it was a computer glitch on their part. I had to get him the direct express card for his social security after that. I had to sell some of our furniture just to pay them and the monthly bills for 2 months.

The problem with the fees on being over withdrawn, started by people scamming the bank and writing bad checks.

They were sometimes using the system to ” loan” them money to pay a check that was not funded, when written. Sometimes they never paid the bank back, but just moved their banking elsewhere. Leaving the Bank holding the bad debts.

So although it is a bad system, it was bad people who caused it to occur.

And though it is less of a expense today, the charge at one time offset the costs of readjusting the totals in the accounts of the merchants the bad checks were written to. Today with computers those expenses are minimal, but it still does cost to process and mail the bad check back to the merchant.

In many places writing a ” bad” check, that is not paid by the bank will get you arrested and prosecuted.

If you make an occasional mistake and cover it the next day, many places will remove the overdrawn charge, if ask to do so.

Now the also offer services to cover you in case of a mistake, like shifting funds from savings or a “overdrawn” loan.

So if you are paying lots of these fees, it is your own fault and carelessness.

You are incorrect and judgmental.

You have clearly never been so broke that a $20 excess fee meant you couldn’t buy bread and milk for your kids. Do you think people who are struggling to this degree are being offered overdraft loans or that they have savings accounts? I’m talking about paycheck to paycheck, penny by penny.

I was fortunate. I got some excellent opportunities and through hard work and sacrifice, dug myself out of this hole. But not everyone has the good luck that I did, and our current economy is offering fewer and fewer of those opportunities. I have nothing but compassion for people caught in this devastating spiral.

I agree, Daisy. If you have never been in poverty, it is hard to understand how precarious a situation it is. My husband and I came back to the US in 1982 when the country was having a huge recession. (At least in the area we were living in.) There were no jobs. And I do mean NO jobs. We threw newspapers and worked at any low-wage job we could find just to put food on the table.

This is what scares me about the current situation in the US. If we see a time when there are few jobs and inflation hits, it will be deadly. Without an income coming in, things can go south quickly. If there are large amounts of people without money, any area you are living in can get dangerous–rural or urban. Trying to live on what you have as cheaply as possible is a useful skill. Thanks for the tips.

I haven’t used plastic since 2008 and haven’t written but two checks since then. Before that, life was hell. No other words. I cannot get credit now but that is okay. I have nothing but compassion for those in the same hole I was in. In my case, I got an increase in a credit card limit unexpectedly and got lots anof cash, as well as a prepaid visa card. I defaulted on all plastic in 2008-09. Never looked back.

My first job at 17 was at a bank. I’m now almost 70. After a few months I realized there was no way the bank had sufficient funds in the vault to cover everyone’s deposits. I asked the bank manager about it and he gave me a book about banking. This was in 1969. When I finished it I went in to talk to him and I said, “this is a scam!” He laughed! The banking industry as a huge lobby and everything they do is in their best interest. It’s true people wrote checks when they didn’t have funds but these days with electronic banking that’s not happening much. Since they get their money interest free imagine what they make in a day from loans, credit cards, nsf charges etc. Their greed knows no boundaries.

I opted out of the bank overdraft. That means if there is no money in my account then the bank cannot pay the bill. That means zero overdraft fees.

I also do not have or use checks. I just paid off my land 20 years early, but I had made those payments with a cashier check. It stopped a lot of problems with the land collection agency that would say my payment was late when it wasn’t. The bank gets involved with cashier checks. Oh for the record, The Texas Land Commission does sell its notes to a third party. Ask me how I know.

I don’t have a credit card. My husband has a debit card to order online (no credit cards), but I choose not to have a debit card. I have no car payments since I buy used cars. My house is being built as I have money so there is no mortgage.

Payday loans are nothing but legalized loan sharking. While I’ve not been overdrawn (fee income is my nemesis despite working in the financial sector – banks have gotten morbidly obese on fee income), I “supposedly” wrote a payment $.10, yes a dime, short. I had no way to look at an image of my check as electronic processing. I called and complained loudly. After being a customer for 35+ years, I did get them to waive their $10 “late payment” fee.

Overdraft protection keeps people, especially seniors, in the perpetual hole. While I won’t go into details, my poor aunt was generously increasing to her credit unions bottom line, largely due to her deadbeat kid.

Just under 10 years ago, I moved out into my own apartment in preparation for a divorce. There were two things I did right away – one was to have a savings account attached to my checking account, stocked with $500. That was (at the time) my emergency fund. Not much, but at least I could afford a $500 emergency, unlike most people today. The second thing I did was to keep $100 cash in an envelope at home. That was my “oops” money (oops, just ran out of gas and it’s 3 days to payday, etc.). Need to buy a couple of groceries or a few gallons of gas? Pull out a $20 and there you go. Of course, I’d replenish it come payday.

It took me several years of working two or sometimes three jobs, but I got out of the hole. I also had to skimp on certain luxuries, like a cheap prepaid cell phone, rabbit ears for the TV (when I actually had time to watch it), and taking my laptop to places with free WiFi to surf the web. But I got it done.

I’ve been close to rich and so broke I couldn’t buy food. Poverty is hard. I lost a home I loved. I almost lost a grown son. Taking him back into my home and taking him to 5 or more appointment per week in a nearby city broke us.

Today we live on Social Security. It doesn’t go far but we’re making it by gardening and careful planning. I have a cash emergency fund but it isn’t enough to repair a much needed pickup truck with a blown head gasket. It may make a down payment with a neighbor hood garage.

We haven’t taken other government help and won’t. Ok call it pride. But we will make it. I grow a big garden so I can dry or can enough to buy very little more. I have ducks, chickens and rabbits and grow a portion of their food so I don’t have to buy it all.

Currently I’m adding berries and other fruits. Those are the hardest things for us get. Seeds aren’t free but aren’t terribly expensive either. Garden huckleberries and strawberry plants will both bare this year. The strawberries will last a minimum of three years and if they make runners they will last many years.

I enjoy growing things so it doesn’t feel like work. It is a joy. Doing you’re best is all you can do. If you’re ignoring planning or saving when its possible then you’re asking for trouble. If you’re trying. Sometimes that’s all you can do.

I never signed up for overdraft protection to begin with. Back when I had a landline, the phone company ran a check by phone (which I never requested or authorized) 10 times when I called to see why my check hadn’t been posted. My bank did away with the charges altogether, as the phone company was known for such things. Phone company refused to acknowledge their errors. I’ve had a cell phone ever since.

Since you wrote this article about 4 years ago, we have seen what the homelessness problem escalated to, especially in California. If you cited the source for the criminalization of homelessness, I missed it. I’d be very interested to know where it came from.

Yes, there are many innocent homeless people – like the victims of Hurricane Helene – who are in that situation due to no fault of their own. As a society, I believe it’s our duty to help them. But what’s happening in California is not that. It’s mostly drug and mental illness related. If you’ve ever dealt with a loved one who uses drugs, then you know that it’s almost impossible to help them until they want to change and it drags down almost everyone around them.

Our country’s approach to the problem is unfair to normal society (yes, I went there. Normal society, because without a norm there is only chaos) to have to dodge panhandlers, drug needles and crap on the sidewalk. What has happened in America is a vile abomination and it has many sources. It has been exacerbated by tender hearts, like mine at times, who put money in the cup of a drug user or advocate/vote for letting them do whatever they want, wherever they want. No one wants to live around that. It will kill businesses, decimate property values and pave the way for destroyed lives.

Homeless shelters? Yes, but regulated and controlled. For veterans and families with children and the elderly, first. For the young and healthy but drug addicted, no. It’s not helping them. Homes for the mentally ill? Yes.

My family has had issues with homelessness dating back to at least the 1920s. My favorite uncle and his family were left stranded about 100 miles from the rest of the family, homeless and broke with no car during the 1930s. His greedy brother-in-law got him fired (because no 2 family members were allowed to work for the company). They carried their belongings out into the woods, and camped, walking miles to a grocery store every few days. Through God’s mercy, they were eventually allowed to live in an abandoned farm house with my uncle working for the farmer. But he was never really stable after that. He worked hard on his own garden and taking care of his own things, but never again kept a steady job and semi-depended on family for the rest of his life.