(Psst: The FTC wants me to remind you that this website contains affiliate links. That means if you make a purchase from a link you click on, I might receive a small commission. This does not increase the price you’ll pay for that item nor does it decrease the awesomeness of the item. ~ Daisy)

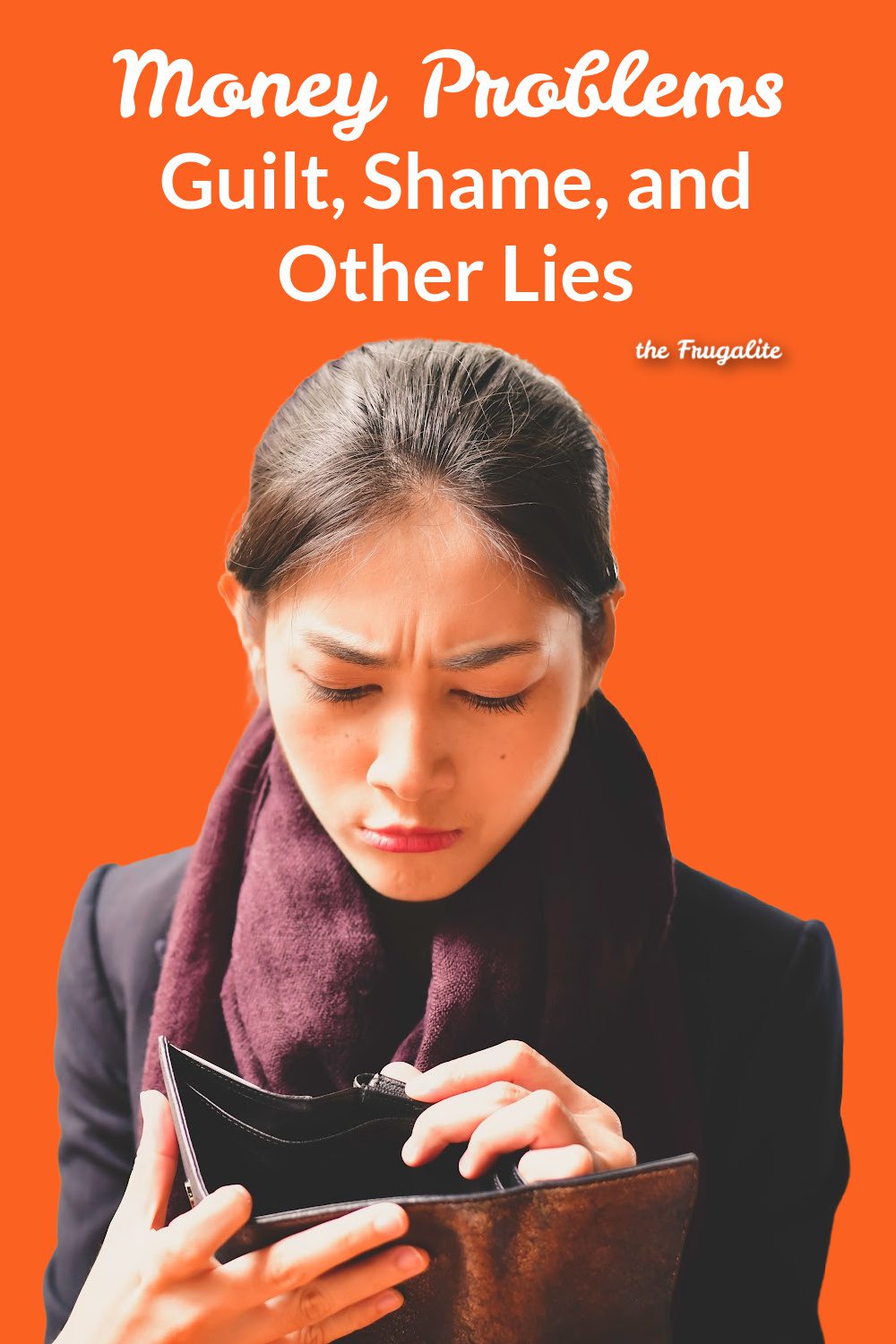

There’s something about suffering from money problems that bring up feelings of guilt and shame. Sometimes those feelings are self-inflicted, and other times, they’re caused by other people, whether intentionally or accidentally. Nearly always, guilt and shame are built on lies that our brain is telling us.

This isn’t true of every single person who has had financial difficulties, of course. All of our psyches are different. Poverty and money problems are universal dilemmas that can happen to anyone, and that’s the brutal truth that most folks don’t want to believe. Financial distress is accompanied by guilt, shame, and all sorts of other lies.

You may read this and wonder why on earth someone who writes about frugality is talking about these experiences. Why doesn’t she have her sh*t together? Why is she having trouble with money and if she is, why am I reading this site for advice? I totally get it. I practice what I preach but any of us can get into a tight spot, particularly in the current economy. If this is not relatable to you, I hope you can find inspiration in other articles on this website.

Why do we feel guilt or shame when money is tight?

When my output is higher than my income, I feel an entire gamut of negative emotions. It’s like running a gauntlet with one side of my head telling me I should have done better and the other side of my head saying, hey, stop that. Things happen.

Maybe it’s because I grew up in a family where everyone was well-to-do and if there were money issues, I certainly never knew of them. Perhaps it’s because I have been so rock-bottom poor as to have dug through dumpsters to feed my toddler. It could be because I’ve fought my way out of deep, dark holes of poverty on more than one occasion and the idea of going back to that place scares me. (You can read about my experiences with extreme poverty in this free book.)

Sometimes it’s other people who make us feel terrible

It’s important to think about the psychology of why they do that. It’s my opinion that if they can convince themselves that your financial problems are completely your own fault and you have nobody but yourself to blame, then those problems can never happen to them. Because they would never make the mistakes you did. It’s like an imaginary cloak of safety when they can believe it’s all your fault.

But the reasons why we have these feelings don’t really matter, do they?

The fact is, many of us feel them. We can’t make our feelings simply not happen, but we can learn to manage them in a healthier way.

Negative emotions surrounding finances can have physical consequences.

I know that guilt and shame, for me, can turn a financial crunch into a physical health trigger due to the whole soup-pot filled with a mix of bubbling emotions.

When I feel those feelings, I throw myself into work, telling myself I will not rest until I fix it. I work relentlessly, day and night, putting in 14-16 hour days in front of the laptop until the letters are too blurred for my tired eyes to continue. I push myself far beyond what is healthy and I do it 7 days a week, never really stopping until I simply am too exhausted to keep going. Then I fall into bed, toss and turn for a few hours, and get up to do it all over again.

Obviously, this is not a recommendation.

What are the results?

- My joints start aching because I’m not out walking a few miles a day with my dog or doing yoga.

- My back and neck hurt from sitting at the computer for such long periods of time.

- I don’t eat well because I don’t stop long enough to prepare myself healthy meals.

- My eyelid starts twitching obnoxiously.

- My stomach aches from the coffee consumption that fuels me.

- I don’t drink enough water because water doesn’t give me an unhealthy spike of energy.

- Sleep, which is nearly always elusive for me, becomes nearly impossible.

And then, eventually, my body says to me, “Okay, I asked you for a break and you didn’t give it to me, so now I’m going to force you to.” And I get sick which often costs even more money that I don’t have.

Sound familiar to any of you?

Then there’s the mental health aspect of financial problems.

We’ve published content about this before in this article. It can often be a chicken or the egg scenario. Your financial problems lead to stress that leads to unwise spending that leads to stress that leads to… you get the idea.

But that’s not all. The guilt and shame attached to it are hard on us.

Maybe some of the following will ring a bell.

- How you feel when you can’t pay for something your child really wants, like piano lessons or a school outing

- The embarrassment of having to make an excuse to avoid social obligations because you certainly can’t swing paying for “your round” of drinks

- Thinking back over every single dime you’ve spent during the last 6 months and feeling bad about 98% of it – did you really need that roast instead of hamburger meat? Did you truly require a new winter coat or could you have mended the old one? WHY did you buy that pizza dinner 3 months ago when you could have made it at home for a fraction of the price?

- The way a family member or friend looks at you with either pity or disdain and you imagine the negative dialogue about you that is going on inside their heads

- The family member that makes no bones about telling you that it’s all your fault

- The complete stranger who smugly suggests that maybe if you didn’t have tattoos (that you got 10 years ago when things were flush) or use a cell phone (that you bought used but they don’t know it) or manicured fingernails (that your kid in cosmetology school did for practice) that then you’d have the money to do whatever it is they feel you should be doing

Those thoughts and more ring in your head like a gong

The berating thoughts echo all the ways you could have avoided this situation if you’d only been better, smarter, wiser, thriftier, or more austere. You feel guilty for not “doing better.” You feel ashamed for not having made “the right choices.”

Soon, your house is a mess because you work constantly and don’t have the time, inclination, or energy to clean it. You can’t sleep because you lie in bed and ruminate over your financial sins. Furthermore, you don’t want to be around other people, even people you care about, because you’re freaking embarrassed about your situation. You turn down invitations to things you’d enjoy because “what if someone finds out?” Your financial problem becomes a dirty, dangerous little secret in your head.

And now, on top of everything, you’re depressed, angry, anxious, and perhaps even a bit agoraphobic.

How do you stop this cycle?

Financial problems are becoming far more prevalent but that doesn’t mean people are being forthcoming about talking about them. Your next-door neighbor or cranky uncle might be just as badly off as you, but they’re trying to hide it so they can feel better than someone else, and thus, better about themselves. Your cousin or your friend might be just as embarrassed as you and not mention it due to the fear of being judged.

- Talk to someone. If you have someone trusted that you can talk to, who won’t be full of “I told you so’s” or “I don’t have any money to lend you” the minute you open your mouth (not that you were even asking), talk to them. A problem shared is a lighter burden to bear and they might be able to help with some good ideas. If you don’t have a person like that, a member of the clergy at your church might provide a sympathetic ear and even resources in a desperate situation.

- Don’t be too proud to accept help. If there’s someone offering you a hand up without strings attached, for crying out loud, take it. As well, remember that you have worked and paid taxes and are every bit as entitled – actually more so – to any help offered by the government as people who use that assistance as their career.

- Stop beating yourself up. Seriously. It’s so easy to just beat the crap out of yourself mentally for ending up where you are but it’s not going to help you to get out of it. When you catch yourself devolving into the whirlpool of negative self-talk that will surely drag you down even further, STOP. Let the other, kinder part of your brain remind you that you are human, you may have made mistakes, or you may just be in a situation beyond your control.

You feel like you are completely alone in this, but I promise you are not.

- Remember that our country is on the verge of economic collapse. Lots of people think of economic collapse as this one huge disaster that occurs on a certain date that wipes out everyone’s finances. In truth, it’s a slow slide of lots and lots of people just like us who either get hit with one big, unexpected expense that takes out their emergency fund and puts them into debt, or whose income can no longer keep up with rising prices. There are more people than ever in your exact situation, but nobody wants to share the story of their self-imposed shame.

- It only takes one thing to go wrong. It just takes one unexpected expense or financial emergency to put you into a terrible spiral from which it feels like there is no escape. And often it happens in bunches. I recently lost a source of income, then had to move twice due to the first home not being in line with city codes, then paid some staggering vet bills before my dog died. Our system is built to kick you when you’re down – suddenly you’re subject to fees and penalties and all sorts of issues. Poverty is a trap that can feel impossible to escape.

Positive steps to overcome guilt and shame

The last thing you might want right now is some Pollyanna bullsh*t about thinking happy thoughts and looking on the bright side. But the fact of the matter is, you can’t hate and berate your way out of financial problems. Making yourself sick physically and mentally will not make your situation better, and will, in fact, make it worse, when your body and brain have had more than enough.

Try taking one or more of the following steps.

- Clean your house. That might be the last thing you feel like doing when you work all the time. But getting things fresh and orderly really will help with your state of mind and will help you not to waste food or let things get ruined. Even if the weather is cold, let a little bit of fresh air circulate and cleanse your space. This is not a waste of time.

- Cook some healthy meals ahead of time. Instead of grimly shoveling Ramen noodles into your mouth, spend one afternoon in the kitchen making nutritious meals that you can heat up during the week. Nourishing your body through this is important because it will help you to remain healthy. You deserve good food. Throw together some generic V-8, either meat or lentils, and some canned veggies to make a soup. Add rice or pasta at serving time. Get some dad-gum veggies into you.

- Give yourself breaks. I’m notoriously bad for working non-stop. It’s my go-to, my way of trying to control a situation that has gone awry. “If I just work harder, I can fix this,” I find myself saying. But, at the advice of an annoying (but very good) friend, I have written 2 hours into my daily schedule to drive to a nearby wooded park and walk my dog. It nearly kills me to do that – I feel so guilty! But I’m doing it and every day, the guilt recedes and my head gets a little bit more clear. While I’m living proof that you definitely can work every single waking hour, I’m also living proof that you should not. For me, the forest or the beach are my happy places. Find yours and make it a hard-and-fast part of your day to go there.

Love, gratitude and stress management

- Spend time with people who build you up. Don’t spend your time with people who tear you down and make you feel even worse about your situation. Those people just underline that negative voice in your head telling you that you are unworthy. Avoid them for now if you can at all, and if you can’t don’t engage on the subject of money. Instead, spend your time with the people who love you for you. Hang out with your children, your loved ones, your very best friends, and allow yourself to feel the love and acceptance you get from them.

- Think about the good things in your life. Colette wrote an awesome article about gratitude journals and the funny thing is, the very worst points of your life are the best time to start them. No matter how dark things are, there are still good things in your life, even if it’s just the bumblebee visiting the flowers on your patio bringing you a smile.

- Find a way to manage your stress. Stress management is essential. You will not get out of your current situation driven sheerly by stress. There are some awesome, thrifty stress management ideas in this article.

Remember that our life has seasons. This might be a dark season for you but it doesn’t mean that a brighter season isn’t still ahead.

How do you cope with money problems?

While we’d all like to think that once we bail ourselves out of financial trouble it will never happen again, that’s simply not the case for many of us. Some don’t make enough money to ensure financial comfort. Others will be hit by some crazy monetary meteor they never saw coming. And again, let me remind you, our economy is in rough shape.

Accepting the fact that this can happen and having a plan to deal with it can really help you when hard times hit. It doesn’t make it painless and stress-free – not by any stretch of the imagination. But it can at least serve as a reminder that just as things can be difficult, they can also get better – and you know this because you’ve done it, my friend.

Have you ever run into serious money problems and suffered from guilt and/or shame? How did you manage it? What coping mechanisms were helpful for you? Did you have any epiphanies during those times that have helped you in the future? Please share your thoughts and stories in the comments.

{kind=link}

7 thoughts on “Money Problems: Guilt, Shame, and Other Lies”

Excellent article!!

I love the compassion n understanding behind this well thought article full of great advice.

I too have ongoing financial difficulties.

My goal is to put away $100 every month for the unforeseen financial difficulties that rear their heads during every year.

In December 2020, I put what I had back into vehicle repairs n maintenance.

Six months later, I had to replace one of those tires due to a huge nail going through it, so that was $170.

Then my dog got stung by bees and had a severe allergic reaction, that was another $250. Knowing it could happen again n bein the Prepper that I am, I spent close to $300 on allergy reaction prevention n meds fir a possible reaction. There went what I had saved back, lol.

Now, four months later, another vehicle repair is taking up what I have put back.

I m still putting money back every month just in case n hope that I reach my goal of having $1000 back for the dog n $1000 for possible vehicle repairs.

I m still hopeful to make it n I m grateful that I did put that money back, so I thank myself for doing the preparation ahead of time when I get to feeling wounded when life throws a stupid my way.

I agree that being out in nature is a great stress reliever. We also go walking n play at a dog park everyday, so those are stress free times n that helps greatly.

One can only do what is possible n try to remember that there are ways through your challenges.

Be positive, give yourself credit, try your best n remember that tomorrow is another day to continue to honor yourself n be the best that you can be regardless of what life throws at you.

Thank you, Daisy

Well done!!

Not speaking about the 1-2% but even those that are comfortable can be in this boat. You work a lot because, yes, you don’t know what tomorrow may bring. Or you think about retirement – have I saved enough, can I stay in my house.

I totally agree accomplishing some small things (like cleaning a room) works – nothing better than a sense of accomplishment.

Senior citizens can have a really hard time asking for help (or making use of assistance programs) – especially those that grew up during the Depression/had Depression-era influences growing up. Far too often years of supporting one (or more) deadbeat child/grandchild is the cause. And when grandma/grandpa have no more money to give, the deadbeats dump them.

And yes, I’ve heard/read plenty of elected officials slam cell phones, tattoos, and/or manicured nails or as I call it, throwing the baby out with the bath water.

Here’s my two cents from my own experience. I got a divorce a few years ago, but prior to that, my now-ex and I went to bankruptcy court for the fourth time (why I didn’t leave her years before that is still a mystery, even to me). In the room before we went up to answer the obligatory questions of the trustee’s office, I noticed that every person (3 or 4 of them) ahead of us had all said that they had declared bankruptcy before. I pointed this out to my now-ex, and she said, I kid you not, “See, we’re normal.” No, that’s not normal. Normal is not knowing what the inside of that room even looks like. That was the last straw. I already knew that I wanted a divorce, which is part of the reason we were even in bankruptcy court, but that remark just sealed it for me.

After the hearing, I went back to work and was visibly shaken. My boss at the time noticed it, and while I don’t remember exactly what was said, I remember showing my frustration and shame at having to declare bankruptcy yet again.

And you talk about stress? That physically manifested itself in my case. The primary reason for getting that divorce was financial (I’m a saver, she’s a spender), though there were other reasons. Before I left her, I suffered from headaches and heartburn on a regular basis, and in the couple of months before I left, I also had pain in the area of my shoulder blade and spasms of tingling down my arm. I popped Excedrin and Tums like candy. In the month after I left, the headaches and heartburn went away and have rarely returned (and usually for good reasons now, like legitimate illness or eating foods that don’t agree with me), and within 3 months the pain and tingling disappeared. That’s what stress, despair and a feeling of hopelessness can do to you.

The first thing I did when I moved out was to put together two emergency funds, as meager as they were. The first was $100 cash in an envelope stored in my lockbox. That was my “oops” money – oops, I ran out of gas a couple of days before payday or whatever. The second was $500 in a savings account that was attached to my checking account, so I could easily transfer money online if I felt I was cutting it too close and could bounce. I’ve increased those dramatically in the intervening years, so the stress and worry is gone, long gone. But it took a lot of work (and multiple jobs) to get there. Never again.

Daisy I love that you are so compassionate!! I’ve been there too, plain macaroni once a day for 3 months.

Raised by grandparents who went through the depression and WWII, very thrifty, paid cash for everything or didn’t buy it.

Hubby and I are on a fixed income, pantry and 2 freezers packed. Chickens and garden. Hopefully those will see us through whatever this country is headed for.

People (friends??) laugh at my preps, canning, dehydrating, etc. Last laugh will be on them.

Keep up your encouraging words!!

I can so relate, both to the poverty and to the blame & shame game that people put on those whose major sin in life is being poor! Always the dig, the jab, the down their nose looks because I couldn’t spend $50 per kid over the course of 10-12 kids, none of whom talked to me outside of Christmas anyway. People can be very cruel.

One thing I found that helped me stay the course was my January 1 ritual: I wrote a road map every year of things I had accomplished over the last year and things I wanted to accomplish over the next. Everything from grow my new business to X point to getting my next level belt in aikido to being able to skip my weekly food bank visit went on that list. I also wrote action items beneath each goal and checked them off as I did them. I kept all of my maps and when I felt down, I read over them to see how far I’d come. It was amazing! I almost wish I’d kept them but when I moved from Seattle back home to Wisconsin, well, one can only pack so much. I’m tempted to reinstate that actually, even though my life is in a much better place.

Treat ourselves with compassion, especially when no one else does. The need is greatest then.

I get the people upset because you didn’t give them good enough gift (& you probably got nothing let alone thank you). My husband always bought his family attention with giving/doing & paying for most things (probably why he had credit card debt & debts with no money even though worked multiple jobs with few bills) & I pulled it back & eventually stopped because we never saw/heard from them unless they wanted something. Yes he made decent money but he also was divorced before me & lived at parents with his kids that he handed cash to on way out door daily. We bought house together, had a baby plus 2 teenager in house & adult child that was never expected to work (I refused to let move into our house but we still somehow still paid some of those bills).

Fast forward 10+ years later & have retirement savings, nice house, good vehicles, able to take 2 week (camping) vacation every year & helped put 2 kids through college while contributing money to 3 of 4 kids weddings. But only because of frugal choices, saying no to giving/buying others/family because they choose different priorities & having a plan for ourselves. Only to find out that husband decides needs other priorities & abandoned/left unexpectedly (last) teenage child & wife (who has not worked outside home 10+ years). He cleans out one retirement account ($20,000+) that spends in 2 months (had not even filed) while living at mommy’s (free) while I still pay all bills.

Thank god I had sense to prep while times were good & that’s only way been able to survive since life changes. Though more life changes are coming I am grateful for being able to not completely hit rock bottom. Hoping to have ability to start again & be able to provide for my teenager & myself.

I was waiting to see if anyone would address some of the external causes of approaching or actual poverty that was not the victim’s fault. I’m reading that today some 60% of American families are living paycheck to paycheck. That did not used to be the case. Part of that has to be the rapidly decreasing purchasing power of money that you’ve earned, saved, inherited, etc. In the 1940s the cost of having a new baby in an American hospital was a little under $100. Today it’s closer to $10,000. That has to be a combination of the Federal Reserve counterfeiting the money supply in addition to the damage done by Lyndon Johnson’s Medicare.

Today the federal spending has jacked up the federal debt into the trillions more than ever before in history. Even though no mainstream media would dare use the correct label of counterfeiting to describe what’s happening … that is the mechanism that steals purchasing power from the population at rates wildly beyond what published tax rates take. The Bank of England was created in the 1690s to do exactly that to help fund the Crown’s foreign wars. There is a hundreds of years history of government’s practice being used in America as well … but no government-approved public school history book dares to tell that truth.

So what can you do if you see the value of your money dropping like a rock? You look at the history of how people coped in countries like Weimar Germany, Hungary, the old Soviet Union, Zimbabwe, Argentina, Venezuela, etc. Survival was a combination of using the local money as little as possible (except for must-do matters), but saving the rest of a person’s funds in some combination of spending to increase one’s earning power, saving funds by starting or buying businesses (where you have the legal right to increase prices as inflation skyrockets), saving purchasing power by acquiring tradeable/barterable goods, saving by investing in untraceable crypto currencies such as Bitcoin or Monero — but only once you learn that how-to, saving purchasing power by acquiring precious metals (gold, silver, etc) by acquiring productive land, or for the already wealthy … acquiring high value art, diamonds and land.

It’s worth understanding what happens to debt during extreme inflation. As the money loses value the debtor gets to pay if off with increasing value dropping money …while the lender takes it on the chin as the payments s/he receives are increasingly worth less and less. That’s why when there is advance warning of skyrocketing inflation on the way, private money lending tends to dry up — as happened in the early 1930s with private home mortgage lenders.

None of this is cause for feeling any personal guilt. This is an an undeclared war from the elites in governments, central banks and the uber-wealthy oligarchs who understand how to profit wildly by using that stolen purchasing power of counterfeited money to quickly acquire valuable assets on the cheap before the ripple effect of such counterfeiting pushes prices sky-high throughout an economy.

–Lewis